Trustage Life Insurance Review

Planning helps take care of your loved ones if something unexpected occurs. Should something happen to you, your family faces both emotional sadness and potential financial difficulties. Life insurance provides crucial support during such a difficult time. It helps cover final expenses and replaces lost income, taking away worries about bills or costs of care. Securing this protection now offers your family much-needed security and reassurance for their future. It all comes down to finding the right insurance service/product.

TruStage sells three life insurance products:

- Whole life insurance

- Guaranteed acceptance whole life insurance

- Term life insurance

In this review, we will take an in-depth look into each of these products so that you can decide whether they are right for you and your family.

First things first, are you eligible for a Trustage life insurance policy?

Stage Eligibility

The first eligibility hurdle is your state of residence.

New York residents are the only ones ineligible for Trustage life insurance policies. Montana and Washington residents are ineligible for one product each – Whole Life Insurance and Guaranteed Acceptance Whole Life Insurance, respectively.

And if you’re a resident of one of the other 47 states, you’re 100% in the clear.

Age Eligibility

The second criterion is age. Trustage life insurance plans are available to individuals between 18 and 85.

For their Whole Life product, eligibility spans this entire range. Trustage’s Term Life product is available to a slightly narrower range – 18 to 69 years old. And finally, Trustage’s guaranteed issue whole-life products have the narrowest age eligibility, offering coverage to individuals between the ages of 45 and 80.

TruStage Life Insurance Terms Table

| Product | Policy Type | Duration | Waiting Period | States Available | Age Range | Coverage Amounts |

| Guaranteed Acceptance Whole Life | Whole Life | Lifetime | 2-year waiting period on payout | All except NY and WA | 45-80 | $2,000 – $20,000 |

| Whole Life | Whole Life | Lifetime | None – Immediate payout eligibility | All except MT and NY | 18-85 | $5,000 – $100,000 (varies by age) |

| Term Life | Term Life | Expires at age 80 | None – Immediate payout eligibility | All except NY | 18-69 | $5,000 – $300,000 |

Coverage Amounts

Each plan’s coverage largely depends on the applicant’s age and selected policy. Here is a breakdown of each of the products and their costs.

- Guaranteed Acceptance Whole Life: The coverage for this plan ranges from $2,000 to $20,000

- Whole Life: TruStage’s simplified issue whole life insurance plan offers coverage whose minimum is $5,000 and whose maximum varies based on the applicant’s age

- Ages 18-70 qualify for up to $100,000

- Ages 71-75for up to $50,000

- And those between 75-86 are able to get up to $25,000 of whole-life coverage

- Term Life: TruStage offers term life insurance coverage between $10,000 and $300,000. Note that these are annually renewable policies, which means that they do not have a defined “term”. Instead, they are automatically renewed each year.

Death Benefit Terms

Guaranteed Acceptance Whole Life Insurance Plan

As with all guaranteed issue policies, TruStage’s guaranteed acceptance whole life insurance policies have a two-year waiting period. This means that, if you pass during the first two years of your policy, TruStage will simply refund your premiums (with 10% interest); they will NOT pay out your full death benefit. After two years, however, your policy will pay out its full face value.

Simplified Issue Whole Life Insurance Plan

The simplified issue whole insurance plan has different death benefit terms than the guaranteed acceptance plan. In this option, the full death benefit is paid to the beneficiaries upon the insured’s passing, no matter when the insured passes. In other words, this plan has no waiting period.

Term Life Insurance Plan

For applicants who select TruStage’s increasing term life insurance plan, TruStage guarantees the death benefit as long as the plan remains active and all premiums are paid in full. Be sure to note that this plan expires at age 80.

See how much you could save

Compare rates from 19 carriers in 60 seconds

Cash Value

Guaranteed Acceptance Whole Life Plan

TruStage’s guaranteed issue plan builds cash value after the two-year waiting period. The insured can access this built-up cash value via policy loans and partial withdrawals. The cash value builds up at a guaranteed interest rate while the plan is active.

Simplified Issue Whole Life Plan

The simplified issue plan builds cash value in the same way as the guaranteed acceptance plan. TruStage deposits a small portion of each premium payment into your cash value account. (You can think of a cash value account as a savings account within your policy.) Over time, your cash value will grow (tax-deferred) at a guaranteed interest rate.

However, TruStage will settle any outstanding amounts at your death from the death benefit they pay to your beneficiaries.

Increasing Premium Term Life Plan

TruStage’s term life insurance does not build cash value, unlike the other coverage options. All premiums go directly towards paying for your death benefit.

Available Riders

Riders are essentially “add-on” coverage that many life insurers offer to “sweeten the deal” and get people to buy their policies. TruStage, however, does not offer any policy riders.

| Rider Name | Plan | Free or Extra Cost | Description |

| N/A | Guaranteed Acceptance Whole Life | N/A | This plan does not offer any additional riders. |

| N/A | Simplified Issue Whole Life | N/A | This plan does not offer any additional riders. |

| N/A | Increasing Premium Term Life | N/A | This plan does not offer any additional riders. |

TruStage Application Process

TruStage makes it easy for you to begin your application on their website.

After you fill out some basic information, TruStage will display your quotes for each of its policies that you are eligible for. It also allows you to quickly toggle your coverage amount, which we found to be a particularly convenient feature.

The formal application took us 13 minutes and involved responding to basic demographic questions, answering yes-or-no questions about your medical history, and paying for your policy via a bank account.

You can complete your application for coverage options like guaranteed acceptance and simplified whole-life plans fast, efficiently, and in one business day via the digital application. The term life plan, however, required a more extensive application process and medical underwriting, and the approval process can span a few weeks.

Once approved, applicants will gain access to a payment portal to access their policy documents and make payments. As soon as you make your first premium payment, your policy goes into effect and can be managed entirely through the online portal or with the help of a TruStage phone representative.

How TruStage Will Decide On Your Approval

TruStage’s underwriting criteria depend on the plan you select.

Guaranteed whole life insurance plans are, of course, guaranteed, so approval is instant.

Simplified issue policies are typically approved within 30 minutes, given that medical underwriting involves only an automated check of your prescription drug history.

If you are applying for a term life insurance policy, on the other hand, it may take a couple of weeks to receive your decision, as you first have to take a medical exam, and then your fluids have to be analyzed by a lab.

Overall, here are the major factors TruStage considers when underwriting your application:

- Age

- Family history

- Health

- Foreign travel

- Avocations

- Driving history

- Financial profile

- Occupation

- Residence

- Tobacco use

TruStage reviews all available information to assess your insurance risk profile and determine your eligibility for coverage.

Paying Your Premiums

Your policy will be active when you make your first premium payment. You can make this payment upfront via the digital portal provided on approval. The payment process is very flexible, offering multiple options to pay your premiums.

Policyholders can pay annually, semi-annually, quarterly, or monthly through automatic deduction. You can view your recurring premium payment in your online portal. Note that the date of each payment will coincide with the day of the month your policy was issued.

Check Out: Is Lumico Life Insurance Worth It?

See how much you could save

Compare rates from 19 carriers in 60 seconds

TruStage Pros and Cons

While TruStage’s plans are flexible, accessible, and affordable, they also come with their fair share of limitations, and this next section breaks down the key positives and negatives to carefully consider before getting one:

TruStage Life Insurance Pros

- No medical exam required: While most life insurance policies need a medical exam (consisting of basic blood/urine analyses up to a treadmill-based stress test!), you don’t have to worry about that with TruStage

- Flat rates: For TruStage’s whole life insurance options, your premiums will remain level for the duration of your policy

- Online application is quick and convenient: The online application process is fast and seamless, making it easy for applicants to get life insurance policies without waiting weeks to underwrite, fill out lengthy forms, or undergo an intimidating medical exam.

TruStage Life Insurance Cons

- Limited coverage value: When you account for inflation, your death benefit may not end up helping much with funeral costs in a decade or two.

- Term coverage expires: TruStage term life insurance policies terminate when the insured passes 80 years old.

- Rate increases: If you have a TruStage term life insurance plan, your premiums will increase every five years

- Waiting Period: Trustage’s guaranteed acceptance plans have a two-year waiting period before they pay out your full death benefit; if you pass during the first two years, TruStage will simply refund your premiums

TruStage Ratings & Reviews

Reviews are a great way to know if a product is right for you. Let’s look into what trusted platform users say about TruStage Life Insurance.

Trustpilot Customer Reviews

Maegan – No Hassle Approval

“The application process was so easy and quick to complete. Within 48 hours, I received an email that my policy had been approved. No hassle, no doctor appointments, no signing over medical records. I am thrilled with the ease and quickness of becoming a TruStage term life insurance policy holder!”

Angela Hunley – Realistic Coverage and Affordable Price

“I had been looking for affordable whole life and longer-term coverage. This company had the best rate and was offered through the credit union at my workplace, where I was already a member. It made the payment process easy with the automatic withdrawal every month.”

William Martin – Lower the price from the age of 60

“Lower the price from age 60 to 80. Expecting those high payments to be easily made after 60 is unrealistic. It’s very unfair after paying ten years that the risk of not being able to pay the premium is a realistic fact.”

Kesha – Customer Service

“I had an issue with billing, and I spoke to a customer service rep, and she cleared up the confusion for me.”

LaRaine Christensen – Rude Salesman and wrong quote on offer

“I received a letter from TruStage offering me a “deal” because I am a Utah First Credit Union member. The letter stated it was as low as $13 a month for $15,000. When I called, the price went up to $80 a month. I am retired and on a fixed income. How do they think a single elderly lady can afford $80 monthly? It is ridiculous.”

BBB Rating

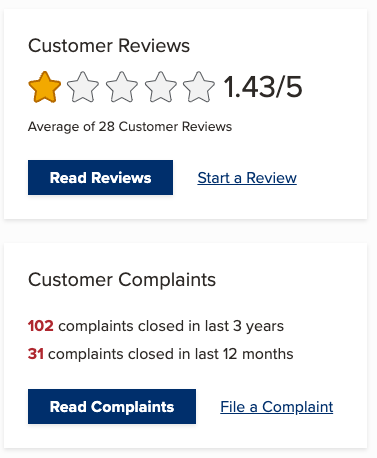

Trustage holds an A+ rating from the Better Business Bureau (BBB). However, they are not accredited, and their customer reviews tell a different story.

Trustage has a 1.43 (out of 5) star rating from BBB customer reviews. They’ve had 102 customer complaints in the last three years and 31 complaints in the last 12 months.

Frequently Asked Questions

What is the application process like?

The application process is fully digital, without any physical paperwork. By filling in a few basic details, you can have your application done in minutes and approval within 48 hours. No medical exam is required—only health and lifestyle-based questions.

How long will it take to receive my policy?

Once approved for a TruStage policy, you will receive your policy documents and insurance I.D. electronically, which you can view and download from your online dashboard. You can also get certified paper copies mailed within one week.

What if I miss a premium payment?

TruStage has a 30-day grace period for missed premium payments for policyholders who opt for the monthly payment schedule.

Can I modify my policy after purchasing?

Yes, you can modify your existing policy after purchase. You may be able to increase your coverage amount through the policy’s rider benefits as long as you continue to meet the insurer’s underwriting standards.

How do my beneficiaries file a life insurance claim?

The beneficiaries can reach out to TruStage customer service, who will, in turn, provide all the necessary details via the claim form. Your beneficiary will submit a death certificate alongside the claim form as proof of the insured’s identity. TruStage will process the claim within three to four weeks.

Rikin Shah

Rikin is the Founder & CEO of GetSure. He is a licensed life and annuity insurance agent (NPN 20214763) in all 50 states plus D.C., with over 15 years of experience in the financial services industry — today focused on helping people compare fixed annuity (MYGA) and CD rates and choose guaranteed savings and income with confidence. He has been featured in publications such as Forbes, USA Today, and U.S. News & World Report, among others. Rikin holds a B.S. in Applied Mathematics from Columbia University and an MBA from The Stanford Graduate School of Business. If you'd like to speak with Rikin about your annuity, savings, or life insurance options, don't hesitate to email him at hello [at] getsure.org.