Does Smoking Void A Life Insurance Policy? [No-BS Answer]

Can you get life insurance if you smoke and how does smoking affect life insurance? What happens if you start smoking after you buy life insurance?

It’s logical to conclude your life insurance company may have an issue with this. Smokers life insurance rates are charged higher monthly premiums given the health risks that come with tobacco use.

As a policyholder with an existing life insurance policy, what are your responsibilities to your life insurer if you pick up a smoking habit post-purchase?

Will you face higher premiums? Will your policy be void if you start smoking?

We’ll tackle these questions and more in this article. Let’s dive in.

See how much you could save

Compare rates from 19 carriers in 60 seconds

Why Do Life Insurers Care About Tobacco Use?

So, what’s the deal with life insurance and smoking?

Few things lower your life expectancy as much as tobacco use.

According to the CDC, over 16 million Americans currently live with a disease caused by smoking. Smoking causes lung cancer, stroke, lung diseases, diabetes, high blood pressure, COPD, emphysema, and heart disease, among many other health conditions.

On top of this, secondhand smoke leads to ~41,000 deaths in non-smoker adults and 400 deaths in infants each year.

As a result, companies are eager to understand your history before offering life insurance policy for smokers. Most companies will require a medical exam if you apply for a medium-to-large policy (> $50,000).

Whether whole life or term life insurance for smokers will always be more expensive than the equivalent policy issued to a non-smoker; however, this has nothing to do with corporate social responsibility or the preferences of Company leadership.

Smokers are at higher risk of death from a variety of causes. Insurance companies have to charge smokers more to compensate for the chance that they may lose money.

Check Out: Should Seniors Consider Final Expense Plans from Open Care?

How Smoking Affects Life Insurance

There are many different ways to consume tobacco, some worse for your health than others, some more addictive than others.

What gives someone a smoker rating for life insurance purposes? After all, many more ways exist to use tobacco and nicotine than to smoke cigarettes.

What Counts As “Smoking”?

Does vaping count as tobacco use for insurance? Yes — smoking involves the use of a wide spectrum of products. Nicotine and tobacco tests for life insurance will be affected by:

- Smoking Cigarettes

- Cigars

- Pipes

- Hookahs

- Chewing tobacco

- E-cigarettes and vapes (nicotine use only)

If you use any of the above, life insurance companies will consider you a “smoker, ” meaning much higher life insurance rates (higher premiums).

How Life Insurers Check for Tobacco Use

Each life insurance company has its underwriting model, driven by unique factors and the weightings of these factors. However, life insurers first screen for tobacco use on the application in all cases.

Smoking Questions On The Application

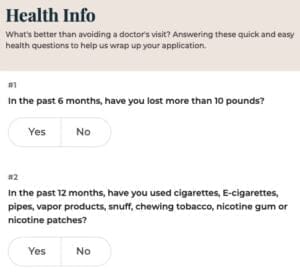

How do life insurance companies know if you smoke? First, they go by your application answers. But they might also do medical exams to determine it, as well as an autopsy once

In the below screenshot, you’ll find the smoking-related question on Bestow’s term life insurance application (Bestow is a digital life insurance agency):

Bestow’s smoking policy is relatively standard. Most insurance companies consider someone a smoker if they have used tobacco-related products within the past 12 months.

However, most make an exception for an occasional celebratory cigar, which they define as no more than 12 cigars within 12 months.

Smoking Detection & The Medical Exam

After the initial screening on the application, most life insurance companies require a medical exam before approving an application and issuing a policy.

The exam will include a urine or blood test for cotinine, a nicotine byproduct. Cotinine remains in urine for three days and in blood for much longer (up to a month) after you stop smoking.

Medical exams are a much more reliable way of both (1) identifying smokers and (2) distinguishing between occasional users vs. those with heavy smoking habits.

Check out: Understanding Life Insurance Coverage for Drug Overdose

See how much you could save

Compare rates from 19 carriers in 60 seconds

Does Smoking Void A Life Insurance Policy?

Life insurance for a smoker is tricky, as your life insurer is betting on your life, literally.

When insurers issue a policy, they are wagering that the insured will stay alive through your term.

The longer you live, the longer you’ll make premium payments to them (and not require them to make a payout).

Likewise, anything you do that lowers your odds of survival is a negative for them. And if your odds decrease enough, your premiums may not be enough to compensate them for the risk of paying out a death benefit to your beneficiaries.

Your Responsibilities (If You Start Smoking)

So, what happens if you start smoking after you buy a life insurance policy?

The answer may surprise you.

If you start smoking after purchasing life insurance, there is NO effect on your policy or premium rate.

While smoking and life insurance are tightly correlated, smoking will not void your life insurance coverage nor can your insurance company change it (e.g., re-classifying you as a smoker and charging you higher premiums).

Your policy and your life insurance company’s obligations to you are 100% unchanged.

A Financial Services Policy That’s Consumer-Friendly?

Some people find this hard to believe. After all, how often do you meet a pro-consumer financial services policy?

Remember, you technically increase and decrease your chances of survival in millions of small ways daily.

If you eat more than the recommended amount of sodium daily, you increase your chances of future health ⓘll; by a minuscule amount. If you drive down the street without wearing your seat belt one morning, you take a slightly greater risk of not surviving your ride (vs. if you had worn your seat belt).

Consumer Habit Change Is Just Another Risk

So the company takes on a lot of risks when they insure you.

And the odds that you would change your lifestyle were a variable! So what if I start smoking after taking term insurance, for example?

Just like the many other choices you make without your life insurance company’s knowledge or approval, you are 100% free to choose to start smoking.

Your life insurance company cannot void your policy, nor can they change your premiums or benefits. Even if your death is blatantly smoking-related, they cannot deny your claim and will still pay out your entire death benefit.

Frequently Asked Questions

Conclusion

Althougho finance companies usually stack things in their favor, this question proves that that’s not always true.

All the more reason to know your rights and policy details regarding financial products.

If you have any additional questions, please comment or email us at [email protected].

Warm Regards,

The GetSure Team

Rikin Shah

Rikin is the Founder & CEO of GetSure. He is a licensed life, accident & health insurance agent in all 50 states (plus D.C.) and has over 15 years of experience in the financial services industry. He has been featured in publications such as Forbes, USA Today, and U.S. News & World Report, among others. Rikin holds a B.S. in Applied Mathematics from Columbia University and an MBA from The Stanford Graduate School of Business. If you'd like to speak with Rikin to discuss your life insurance options or questions, don't hesitate to email him at hello [at] getsure.org.

![How Much Does An Urn Cost? [& How To Save in 2024!]](https://getsure.org/wp-content/uploads/Porcelain-Urn-With-Candles-and-Mourner-1-768x512.jpg)