Not all heroes wear capes.

Some are just ordinary Americans who know a powerful secret about money.

And they use it to save their families thousands.

What's The Secret?

Some are just ordinary Americans who know a powerful secret about money.

And they use it to save their families thousands.

What's The Secret?

* Publications in which GetSure has appeared in 2023.

The Problem

Dying Is Not Cheap...

... In total, American final expenses averaged $17,199 last year*

* "The Cost of Dying in 2023" Report

The Options

Buy Money Now...Or Later

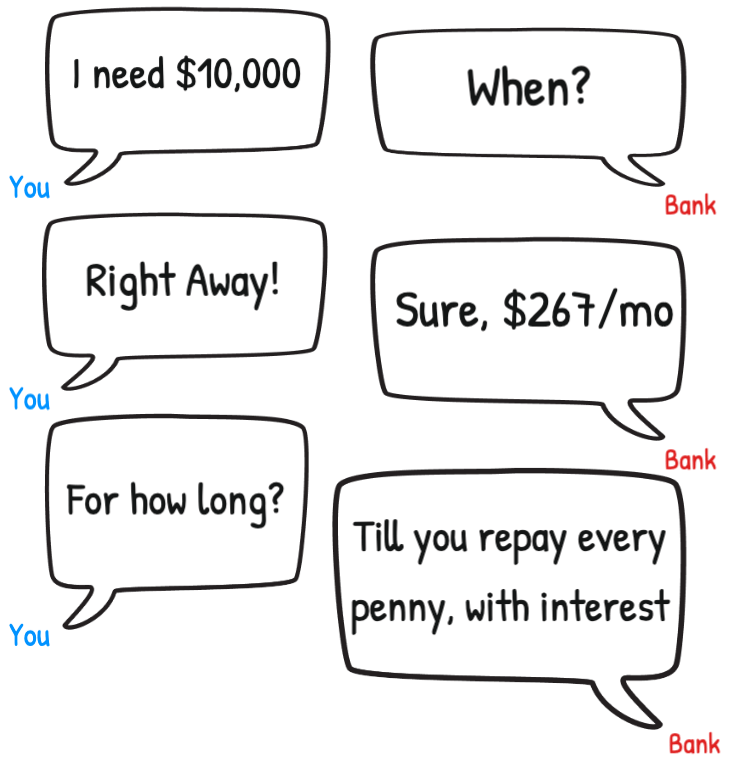

If your family doesn't have $17,199 in savings, someone is going to have to buy money...

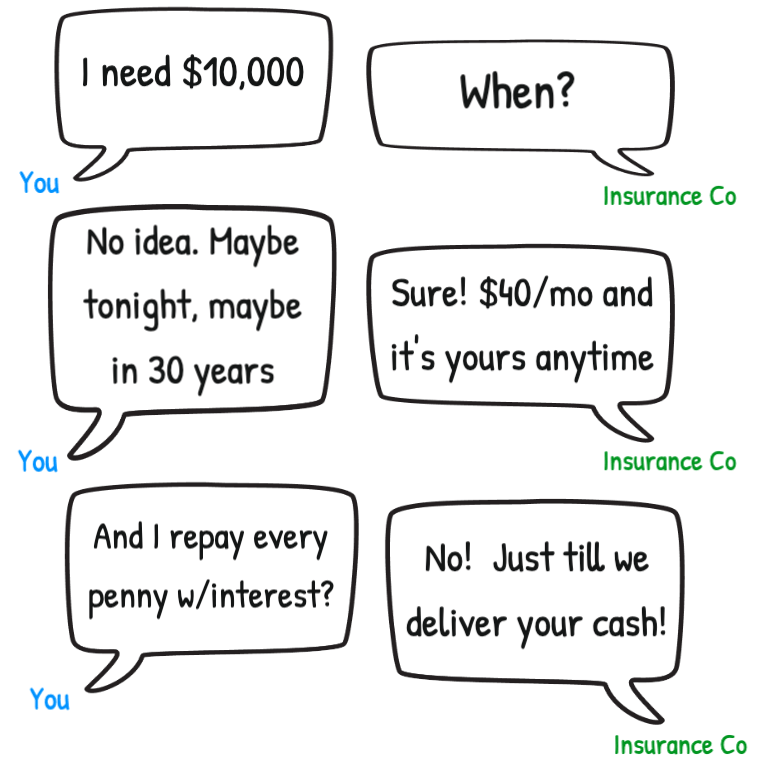

You can

buy money early via

Life Insurance

You can

buy money early via

Life Insurance

They can

buy money

late via

Credit Cards

They can

buy money

late via

Credit Cards

The Secret!

The Reality

Note: It costs the average American $267/month over 60 months to repay $10,000 of credit card debt. That's $15,810.26 in total (source)

Note: Rate is for a 65-year-old woman. Total paid is calculated over her remaining life expectancy (of 19.7 years, according to the Social Security Administration) (source)

The math says insurance beats debt

any day of the week...

And is there a better or fairer

salesman than

math ?

Hello! We’re Martha and Rikin Shah, and we’re thrilled to welcome you to GetSure!

We’re a family business and independent life insurance agency licensed in all 50 states (plus D.C.).

We sell term and whole life insurance to Americans ages 0-90, and we’ve partnered with 19 insurance companies to do so.

Our motto internally is "do

small things with great love". If we have the opportunity to work with you, we hope you'll see that

before long.

Warm regards,

Rikin & Martha Shah

Co-Founders, GetSure

Choose kindness.

You never know what battles people may be fighting.

Explore our 2023 No-BS guide on funeral costs. Find detailed breakdowns by expense type & state, burial...

Let's be honest. Colonial Penn's life insurance is not easy to understand. Check out this rate chart...

How Much Coverage Is The 995 Plan? First, we’ll look at the key question most people want...

AARP has one of the strongest brands in the U.S. But are AARP life insurance rates as...

We'll cut to the chase. Globe Life is expensive and we'll prove it to you by showing...

If you're looking for Mutual of Omaha life insurance rates, then you're in the right place. We...